Cash Value Life Insurance in Retirement Planning

Life insurance provides death benefit protection in the event of a premature death, for any number of needs, including to pay off a mortgage, replace a salary, pay estate and transfer taxes, or fund a college education. But did you also know that life insurance can have living benefits?

The policy’s cash value can grow tax-deferred, and any accumulated cash value can be accessed tax-free via loans and withdrawals, as long as they are properly structured. Moreover, these features can also make the policy cash value a good choice to supplement primary sources of retirement income.

LIFE INSURANCE IN RETIREMENT PROVIDES THE FOLLOWING BENEFITS:

- In the event of premature death during the working years, the income tax-free death benefit can protect the family, replace income, and complete financial obligations.

- The policy’s cash value can be used to help supplement the income from the client’s other retirement assets.

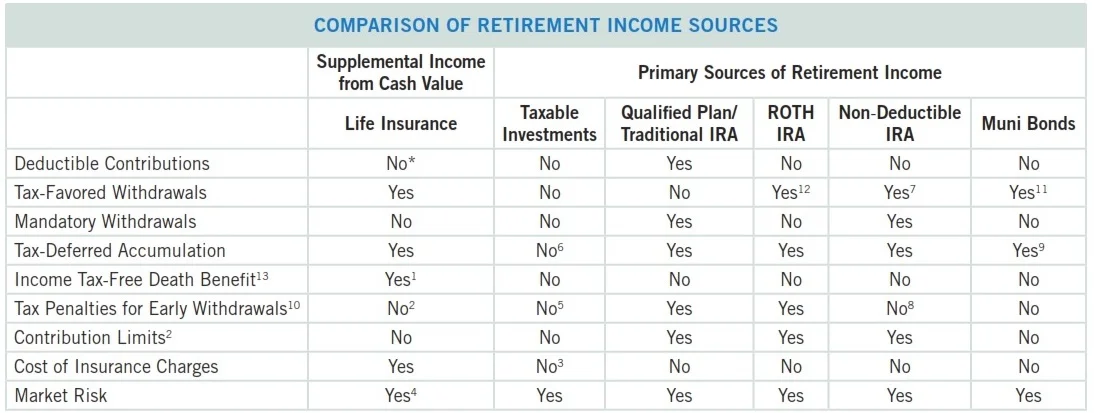

Take a look at the chart below:

This chart outlines some of the important features of a variety of financial vehicles. An understanding of these features may help you to determine which of these products may meet specific needs and whether cash value life insurance can complement an existing financial portfolio.

BENEFITS OF LIFE INSURANCE IN RETIREMENT PLANNING

- The life insurance death benefit will generally be received income tax-free by heirs.

- The life insurance cash values can grow tax-deferred.

- As long as the policy is not a Modified Endowment Contract (MEC), individuals can generally take tax-free withdrawals up to basis out of the policy, and tax-free loans thereafter from the available cash value.

- Accumulated cash value may be accessed by the client or remain in the policy.

Some additional information you may wish to consider:

The primary purpose of life insurance is for death benefit protection, and this strategy assumes this to be a priority objective for the policy owner.

- Life insurance premiums are not tax-deductible.

- Life insurance policies classified as Modified Endowment Contracts (MECs) may be subject to tax when a loan or withdrawal is made, and a federal tax penalty of 10% may also apply to a MEC if the loan or withdrawal is taken prior to age 59½.

- The policy cash value available for loans and withdrawals may be worth more or less than the original investment amount, depending on the performance of the policy crediting rate. Life insurance policies may also have surrender charges in the early policy years. Other factors that will affect cash values are the timely payments of premium and the performance of underlying investment accounts, where applicable.

- Withdrawals and loans can reduce the policy death benefit and cash surrender value and may cause the policy to lapse. Lapse of a life insurance policy can cause the loss of the death benefit. Lapse of a life insurance policy with an outstanding loan may cause adverse income tax consequences.

- For life insurance, the cash value available for loans and withdrawals may be worth more or less than the original premiums paid. Withdrawals from a life insurance policy may be subject to income tax after withdrawals exceed cost basis.

- Taxable investments may be subject to income tax and/or capital gains tax.

- Distributions from non-deductible IRAs must be pro-rated if the client has deductible IRA monies or earnings in the non-deductible IRA.

- Contributions to qualified plans and traditional IRAs may be tax-deductible, subject to certain limits.

- While qualified distributions from a ROTH IRA are generally federal income tax-free, if the ROTH IRA is a rollover IRA, a waiting period may apply before distributions will be tax-free.

- The tax treatment of income from municipal bonds will vary with the type of bond and the issuing municipality.